The Controller's AI Assessment Presentation Template

An 8-slide editable PowerPoint framework for presenting an AI governance and risk assessment to your CFO or CAO. Neutral design — your analysis, your voice, no vendor logos.

This template is a scaffold, not a deck to present as-is. Read through all eight slides below to confirm the framework fits your fact pattern. Then download the PowerPoint, spend thirty minutes filling in your department's specifics, and present a current-state AI assessment that reads as your work — not a vendor pitch.

Step 1 · Review

Scroll through all 8 slides

Confirm the framework is substantive and covers the questions your CFO will ask. No download required to review.

Step 2 · Customize

Download and fill in your specifics

Department name, your findings from the inventory exercise, your specific risk exposures, your materiality thresholds, your vendor evaluation pipeline.

Step 3 · Present

Thirty-minute conversation with the CFO

The framework is designed to end with three questions you pose to the CFO — the answers reveal whether the organization is positioned to govern AI or is about to find out it is not.

Preview · Review all 8 slides

The framework at a glance

Each slide below is the exact content of the downloadable PowerPoint — same layout, same type, same editable design. Placeholders marked [ like this ] are where you fill in your department's specifics.

Slide 1

Framing — "AI is already in our department. Here is our assessment."

The opening that sets the stance. Not a sales pitch. Not alarmism. A considered current-state read from the person who owns the ICFR consequences.

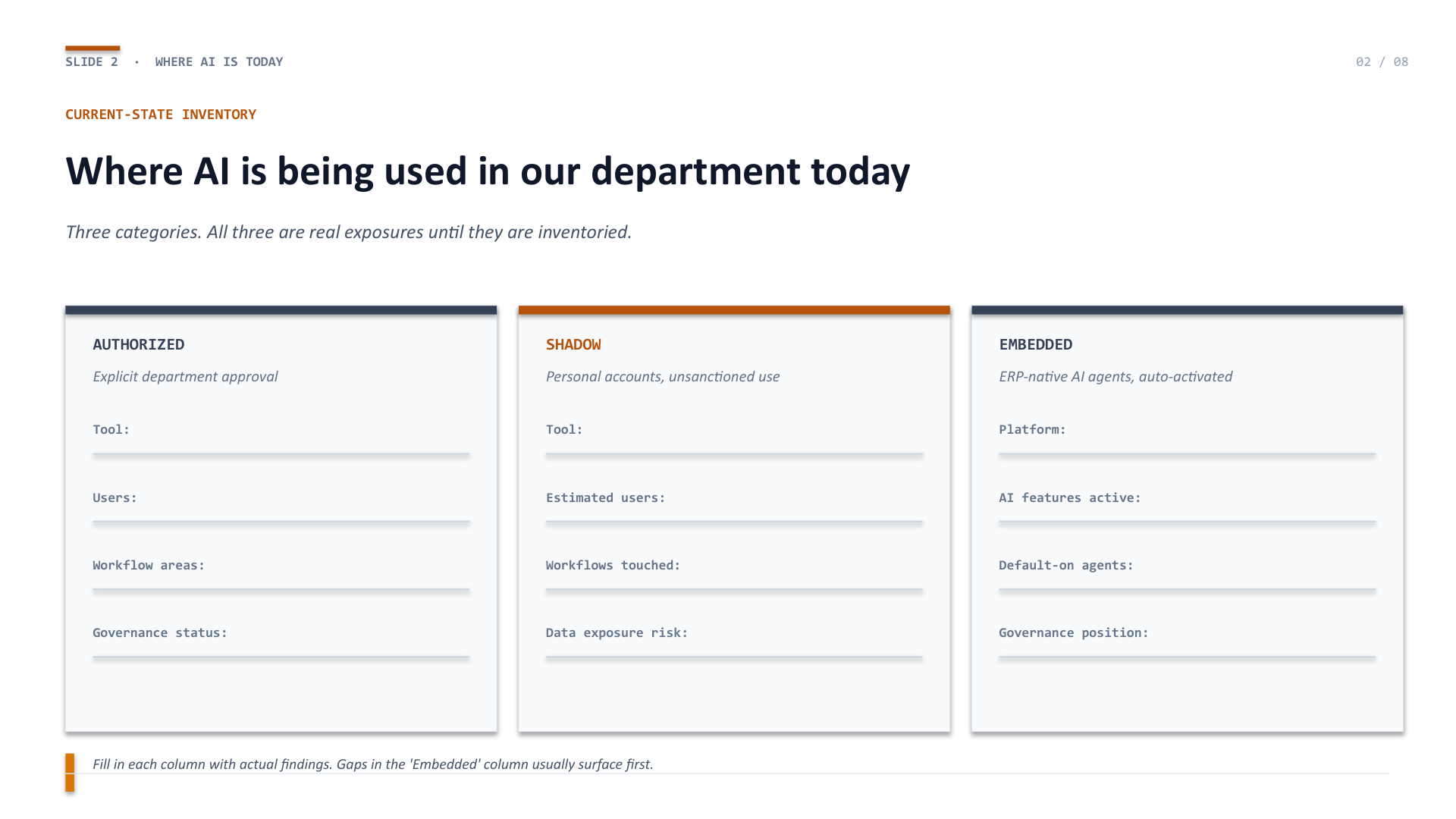

Slide 2

Where AI is being used in our department today

The three-column inventory: Authorized (explicit approval), Shadow (personal accounts, unsanctioned), and Embedded (ERP-native AI agents auto-activated). Most departments have exposure in all three columns without having inventoried any of them.

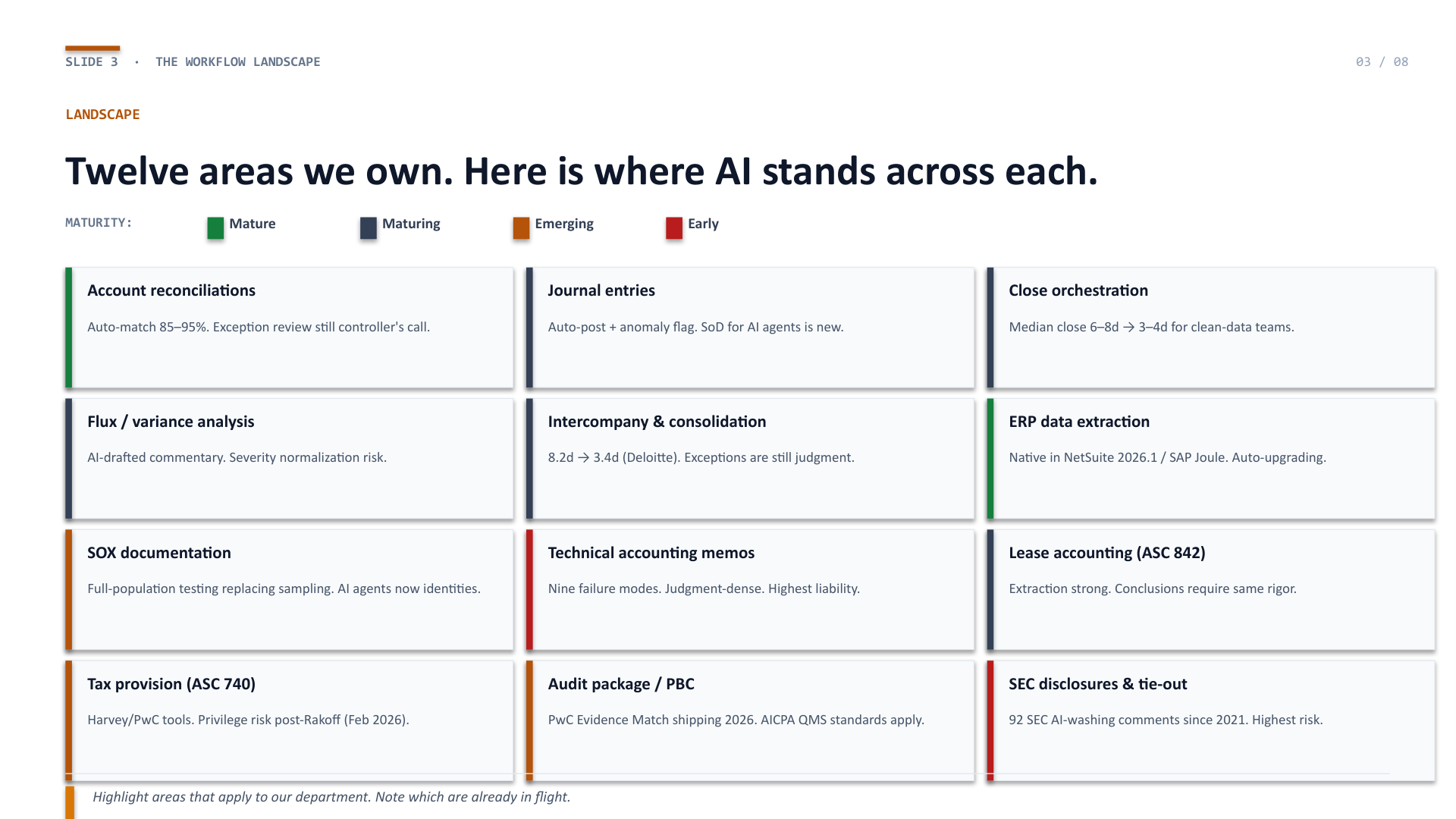

Slide 3

Twelve areas we own. Here is where AI stands across each.

The 12-area workflow landscape from the Hub article, compact, color-coded by maturity grade. Highlight the rows that apply to your department and note which are already in flight. The combination of mature areas and emerging areas is where the governance conversation gets specific.

Slide 4

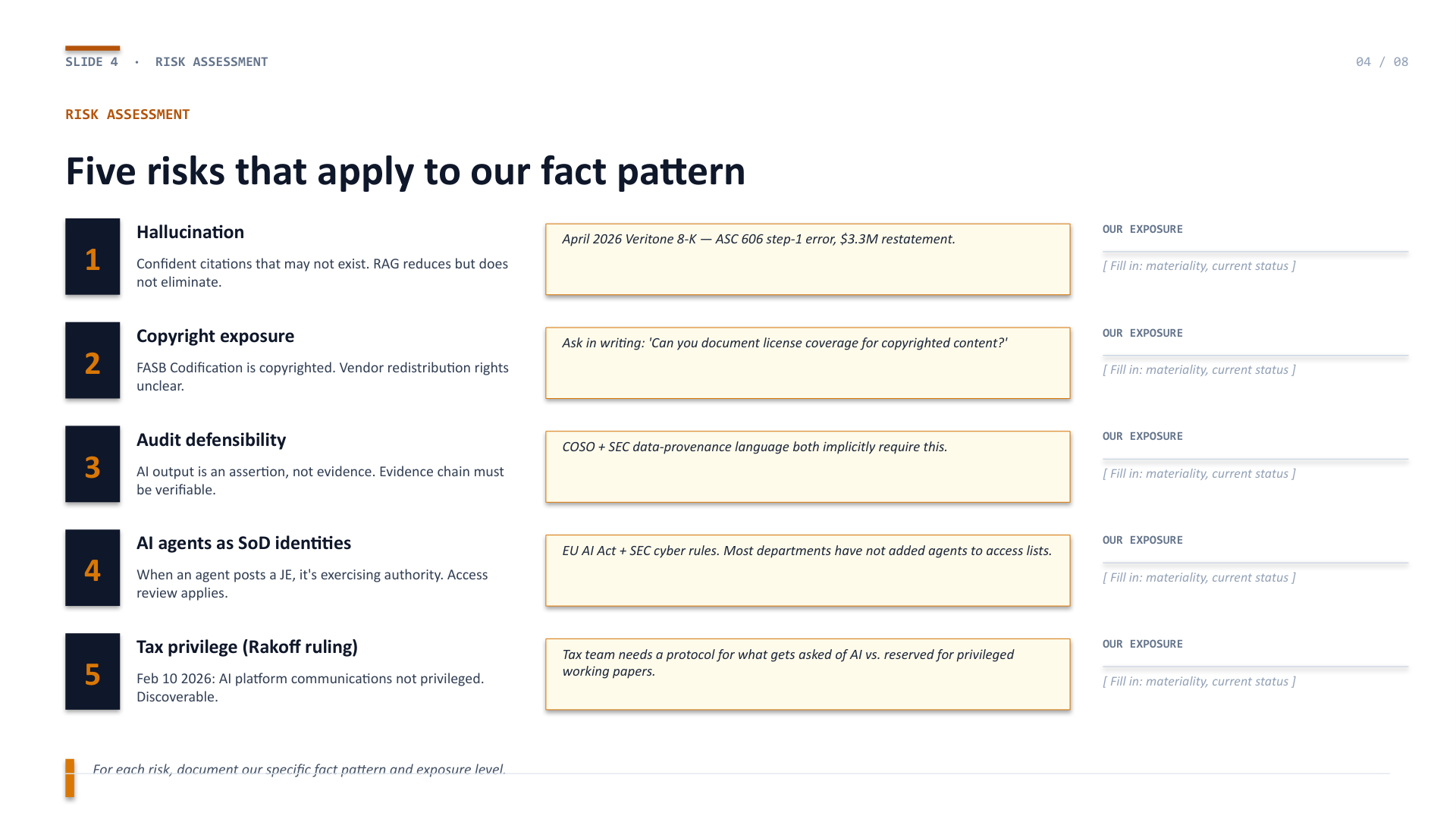

Five risks that apply to our fact pattern

Hallucination, copyright exposure, audit defensibility, AI agents as SoD identities, and the tax privilege wrinkle from the February 2026 Rakoff ruling. Each row includes a specific 2026 evidence point. The rightmost column is where you note your department's exposure and materiality threshold.

Slide 5

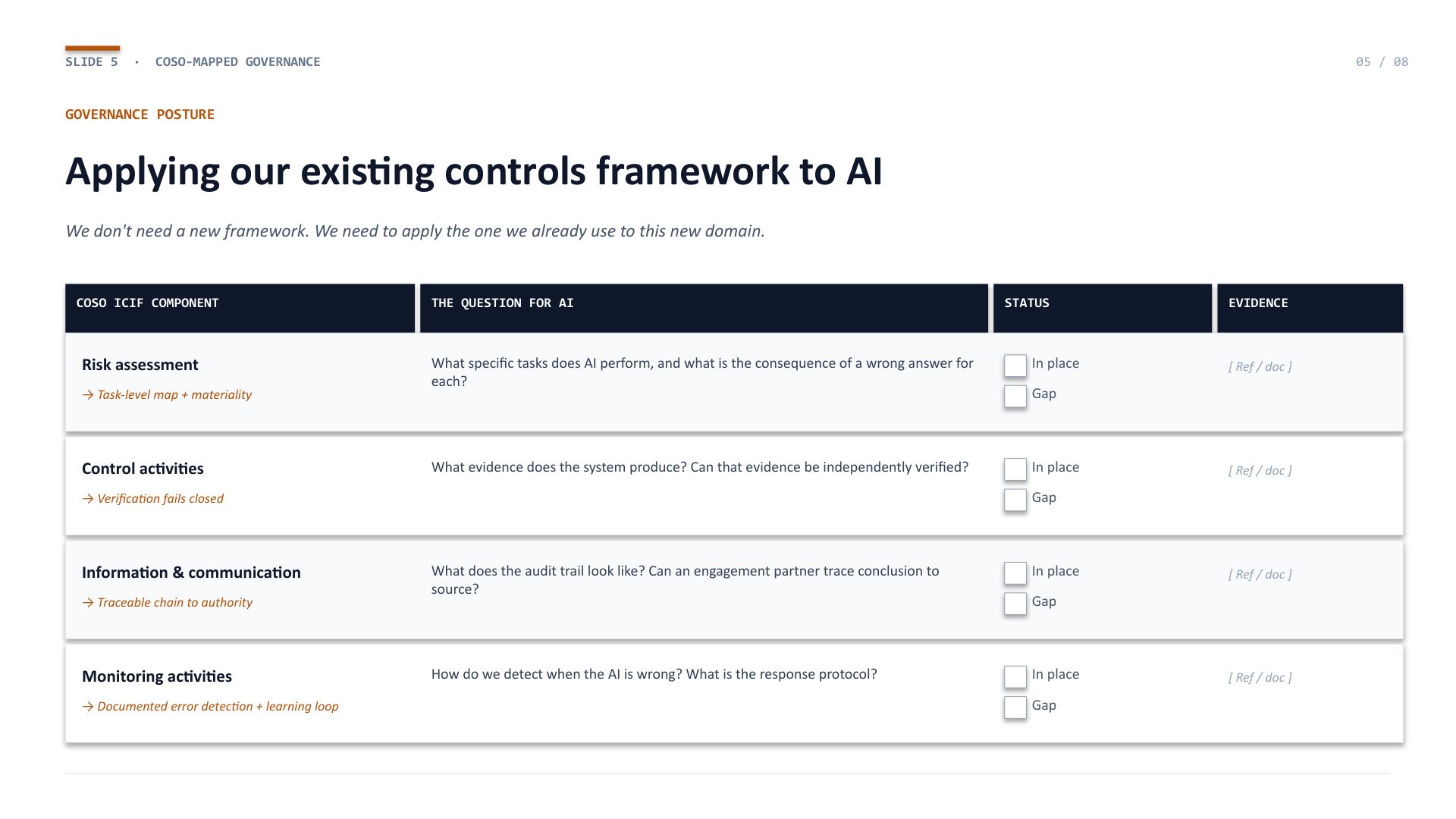

Applying our existing COSO framework to AI

The four COSO ICIF components mapped to the AI-specific question. "In place" / "Gap" checkboxes with an evidence reference column. This is the slide that tells the audit committee you are governing AI the way you govern every other control — not reinventing the framework.

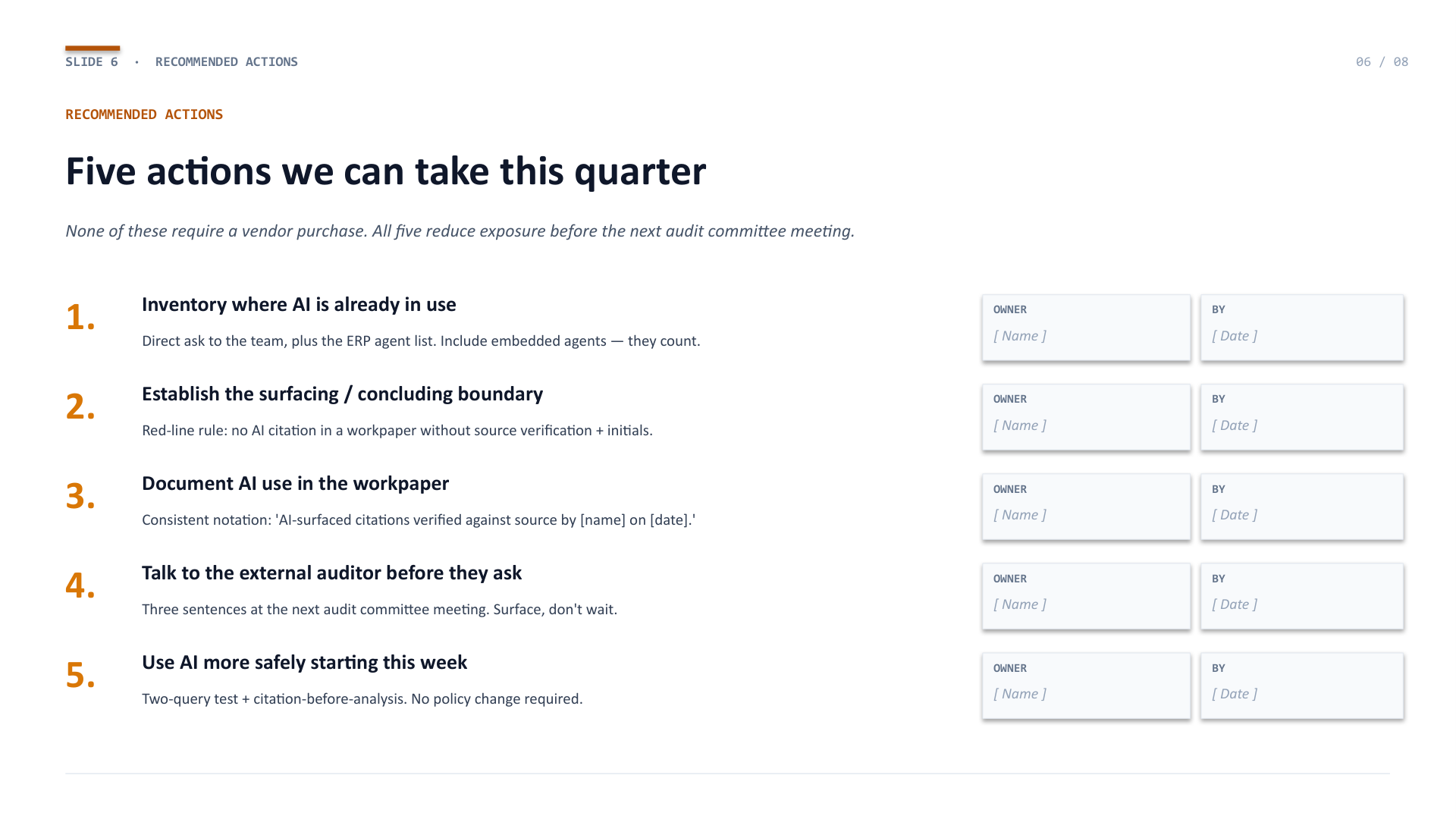

Slide 6

Five actions we can take this quarter

The five quarterly actions from the Hub. None require a vendor purchase. All five reduce exposure before the next audit committee meeting. Owner and target-date fields for each.

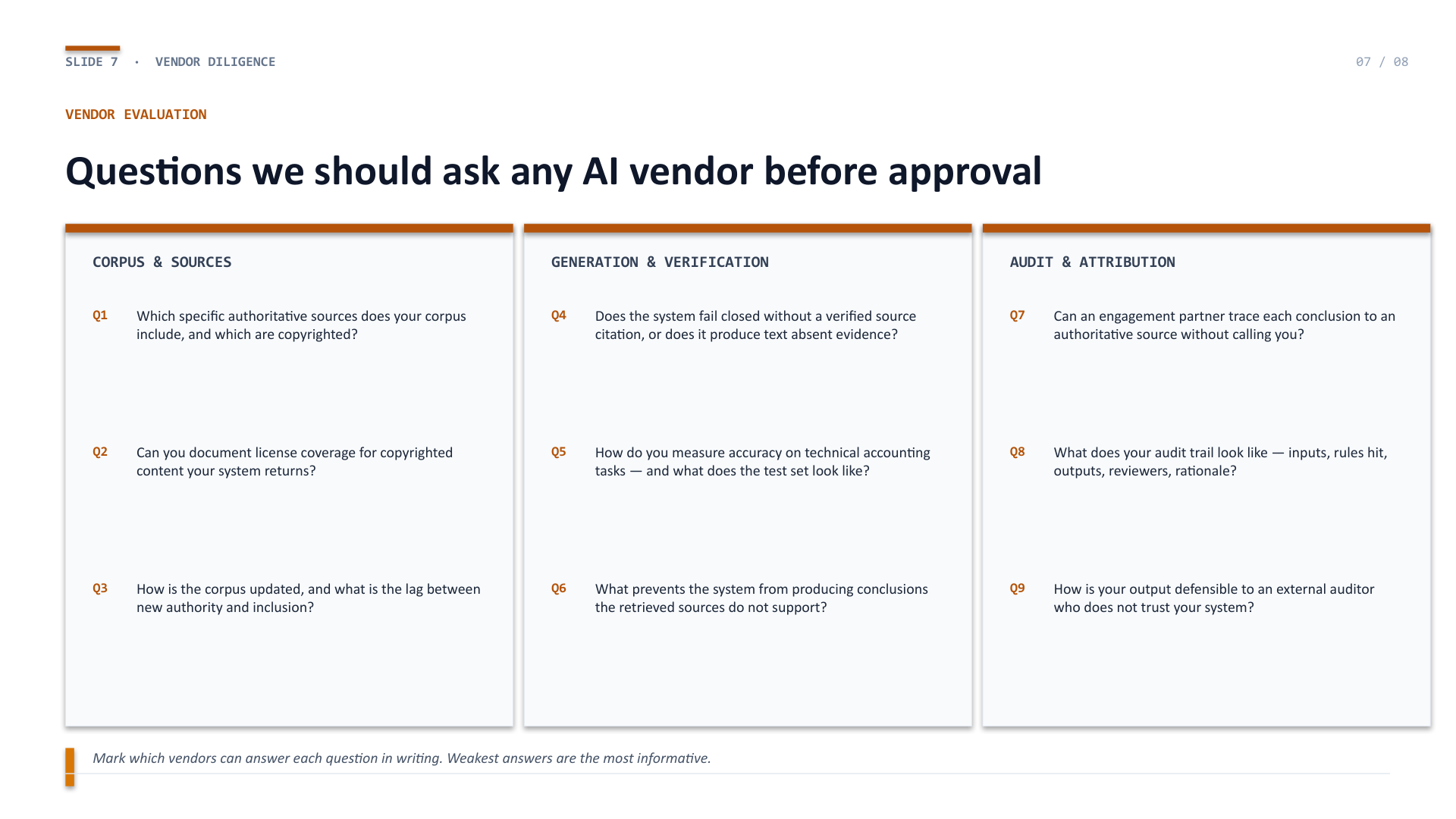

Slide 7

Questions we should ask any AI vendor before approval

The nine vendor diligence questions, organized into three domains: corpus and sources, generation and verification, audit and attribution. A weak answer is as informative as a strong one — the diligence is in the follow-up.

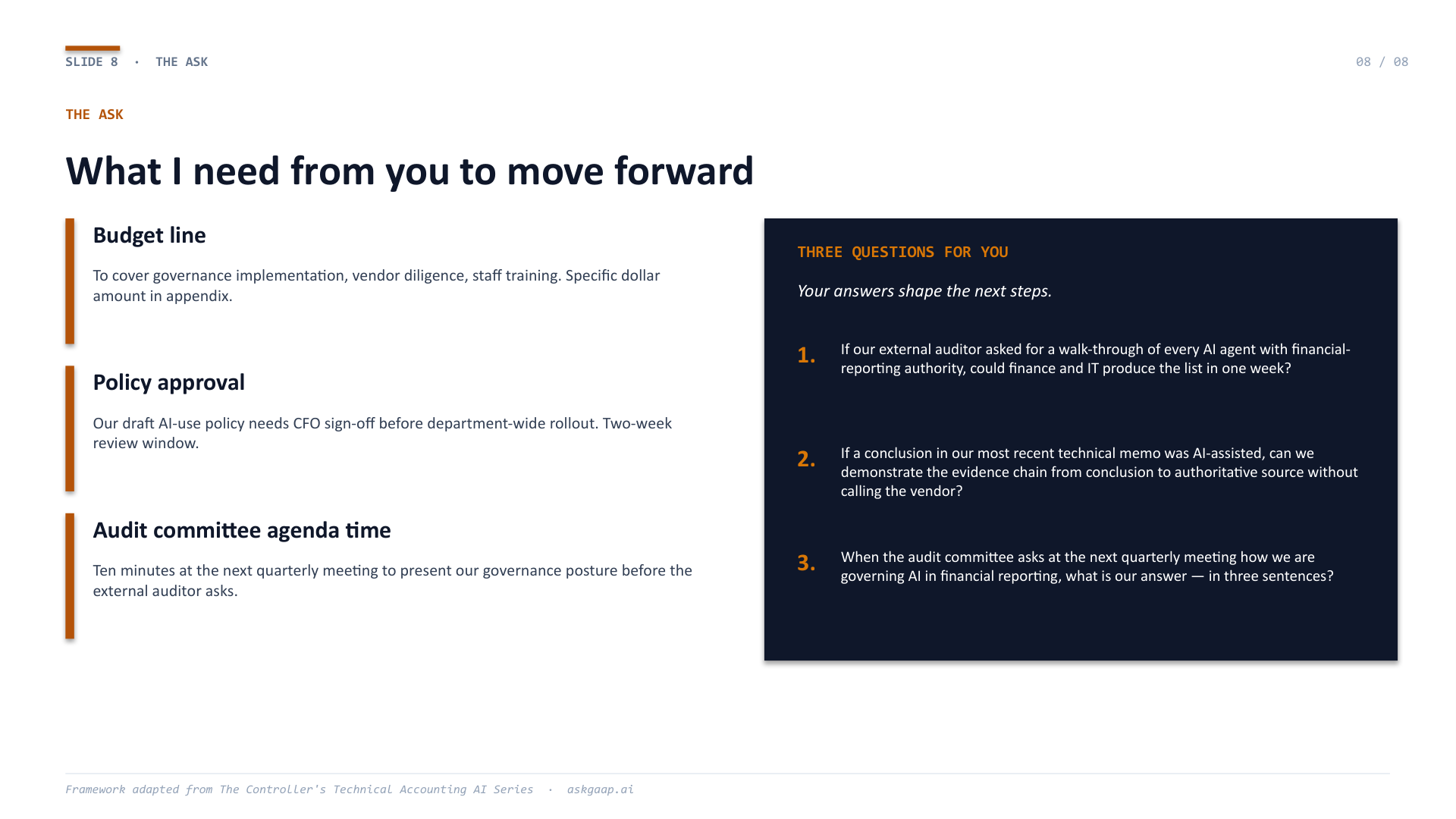

Slide 8

What I need from you to move forward — and three questions for you

The ask (budget line, policy approval, audit committee agenda time) paired with the three questions you leave the CFO to think about. The questions are the most useful part of the presentation. The CFO does not need to answer them today — but they should be the ones asking them before someone else does.

Download the editable PowerPoint

Customize with your department's specifics in under thirty minutes. No email required. No form. No drip campaign. Just the template and a Monday morning deadline.

Ungated · No registration · Editable in PowerPoint · Keynote · Google Slides

Companion to: A Controller's Guide to AI in Technical AccountingThe framework in this template is the practical application of the Hub article. If you arrived here first, the article provides the context and evidence behind every slide.